Small business: The potential pitfalls of growth for growth’s sake

At some point, all small business owners will inevitably deal with pivotal questions surrounding growth. Among the most common headscratchers: What’s the best way to grow my business? And how do I know if I’m heading in the right direction?

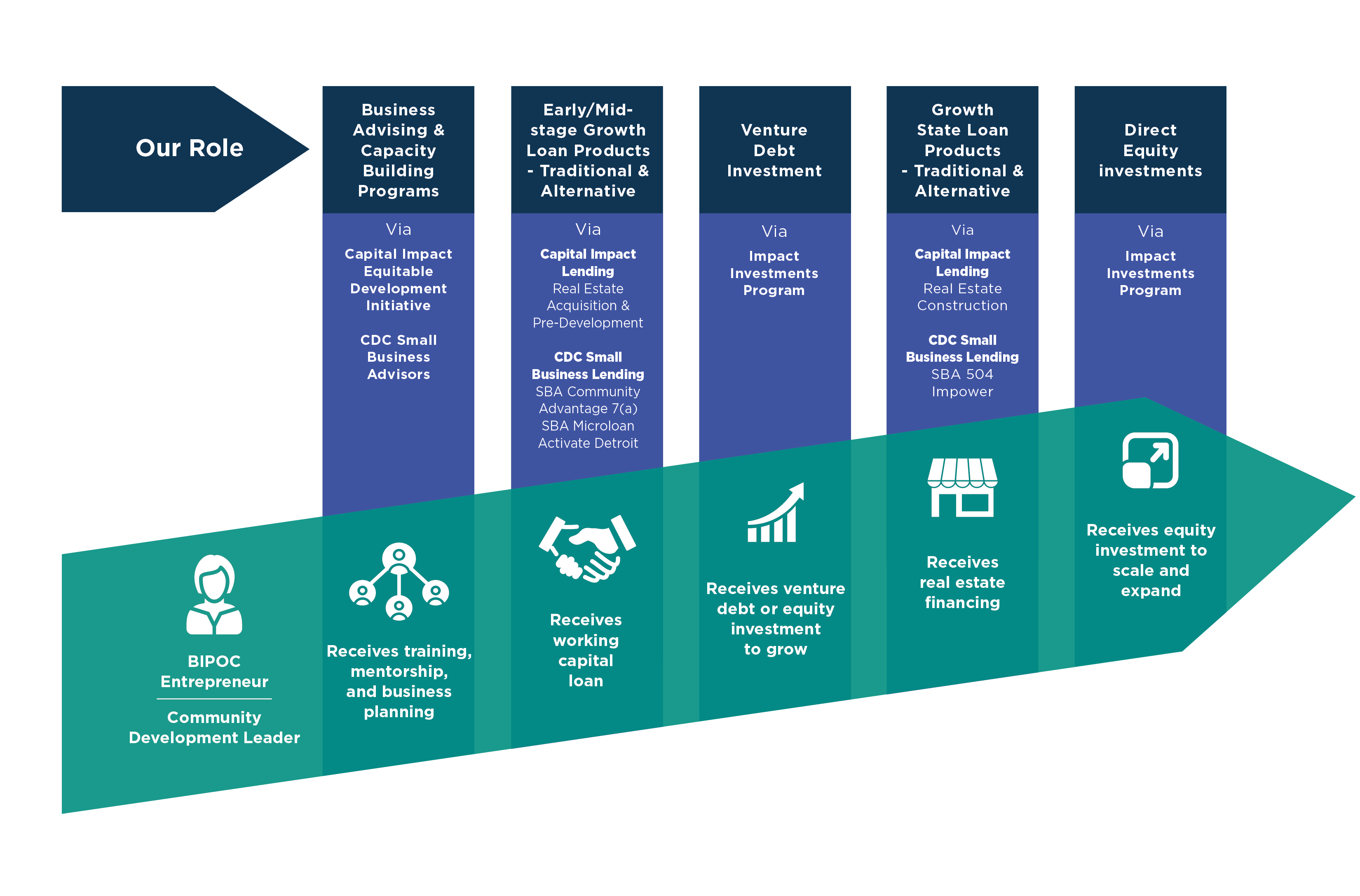

Answers will vary greatly, depending on business type, one’s risk level and personal financial goals, among others. But one thing’s for sure, entrepreneurs often make the mistake of equating just any kind of growth with quality growth, said Antonio Pizano, a financial services veteran at CDC Small Business Finance. CDC is a top U.S. small business lender that works tirelessly to provide funding to underserved communities including women, minorities and military veterans.

We recently sat down with Pizano and Marsel Watts — an experienced, in-house small business advisor — to discuss the nuances of growing a business and how to do it wisely. The following edited interview is part of a new monthly Q&A series with CDC’s expert loan officers and business advisors.

Q: Can you walk me through a common business growth scenario?

Watts: With startups, growth is necessary in order to sustain that business. Their sales in the first several months are probably going to be in the red. After awhile, they may start to see profits. And after that, it depends on where the entrepreneur wants to go. He or she may be at a point where they are satisfied in terms of revenues and sales. They may just be happy with one store or “x” number of customers. It depends on what the business owner wants.

Q: What does growth typically look like?

Watts: Growth can be measured in different ways, from improving one’s service to increasing the number of products. With more products, it means more revenues. But with storefronts, at a certain point, you may have to consider opening up a second location. You’ll see that a lot with franchises. So, in these cases, they can see a larger profit once they have more locations. But the quality of the business could then be affected by growth. But if you don’t expand, then you’re not going to grow. Business growth and maintaining a level of quality go hand-in-hand.

Q: What are some questions small business owners should ask themselves when they experience growth?

Pizano: Business owners should be asking themselves: What were the causes of growth? Was it accidental or strategic? Was the growth due to a certain type of customer or was it a product? Really get down to nitty gritty of the numbers. At CDC Small Business Finance, it’s important for us to understand how and why a business experienced growth. This helps us evaluate if a potential borrower can sustain it and, ultimately, have the ability to repay a loan.

Q: What’s a common mistake small business owners tend to make when they try to expand their business?

Watts: One thing I see is not being prepared to absorb the growth. They may get a big order from a company and then they cannot supply the product the store has requested. Often it’s because they lack the financing to actually develop or buy more inventory. Some ways to prepare for growth are working with a SBDC or business advisor or even researching articles online through many organizations that support small business education. Some ways to prepare for growth are working with a SBDC or business advisor or even researching articles online through many organizations that support small business education.

Pizano: Regarding common mistakes, I’ve seen businesses not prepared for growth or they didn’t have a plan in place. Oftentimes, they think any growth is good growth. And that’s not always the case. Just like lack of business may kill a business, too much growth too fast can kill it, too. For example, you’ll often see businesses underbidding on projects or giving better pricing. They may do it just to make the sale or close the deal and don’t consider the impact of that sale. More often than not, this reduces the margins and the bottom line.

Q: Is this where a predatory loan could come in if the business needs the funds badly enough?

Watts: Yes, if they need the funds immediately, they may go to predatory lenders whose loans have high interest rates. We’ll often see businesses 6-12 months later and they’ve fulfilled the order, but now they’re paying extremely high notes on a loan. If you can’t get traditional financing quickly enough, options in avoiding predatory lenders/high interest rates is to borrow from family, friends, investors, personal line of credit or get a HELOC.

Pizano: In recent years, we’ve experienced an extraordinarily high number of small businesses seeking to refinance and/or consolidate this type of debt. We’ve assisted several businesses get out of these types of loans. We’ve helped them hit the “reset button” by restructuring such debt and providing cashflow relief.

Q: What are some growth challenges when it comes to low-to-moderate income, or LMI, communities?

Watts: The challenge is access to capital in order to get to the next phase of their business. In the LMI community, standards for borrowing are a little challenging mainly due to collateral. More specifically, in California where the cost of living is so high, they either have no equity in real estate or no real estate holdings in general. In this case, they have to build their business slowly, carefully watch their cash flow and return profits back into the business. This is the growing challenge, issue and concern for the LMI community on getting access to capital.

Pizano: Even if they do have the access to capital, these communities tend to be more risk averse or have a lower tolerance to risk. For many, if they fail, that’s their livelihood. They can’t absorb a potential loss like others, who have with more resources. They just don’t have the assets to go “all in.” That may stunt their ability to fund potential growth. Talking to a lender or financial advisor can always help a business owner manage risk. A professional can also assess if a business is in a position to tolerate some growth, to what extent, and how to prepare for it strategically.

Q: Why is it important to lend to these communities?

Watts: The LMI communities are generating revenue and injecting the revenue back into their communities. That helps them thrive and survive.

Pizano: As a community development financial institution, or CDFI, it is one of our primary fundamental objectives to directly invest in and deploy capital in these communities. It’s not only an investment in underserved communities, but it also fosters local job creation and promotes the ‘shop local’ movement. It is common for local residents in such communities to shop at their local food or retail stores. Why do we believe in them? Communities of color tend to patronize local businesses who tend to hire folks from within the same community. These communities don’t need nor do they seek charity. But rather, they need to be empowered by way of capital, investment, and resources. This is all essential to the building of assets and creation of wealth over time

Marsel Watts, a member of CDC’s business advising team, has an extensive background in nonprofits, and business consulting and training. Previously, she was the director of the women’s business center at VEDC (Valley Economic Development Center), a small business lender and nonprofit in Los Angeles. She is passionate about people, entrepreneurs, innovation, and bringing new ideas to the forefront.

Marsel Watts, a member of CDC’s business advising team, has an extensive background in nonprofits, and business consulting and training. Previously, she was the director of the women’s business center at VEDC (Valley Economic Development Center), a small business lender and nonprofit in Los Angeles. She is passionate about people, entrepreneurs, innovation, and bringing new ideas to the forefront.

Contact: mwatts@cdcloans.com

Need financing to start or expand your business this year? Tell our loan experts about your needs, and they’ll work to match you with a financing plan that best suits you.