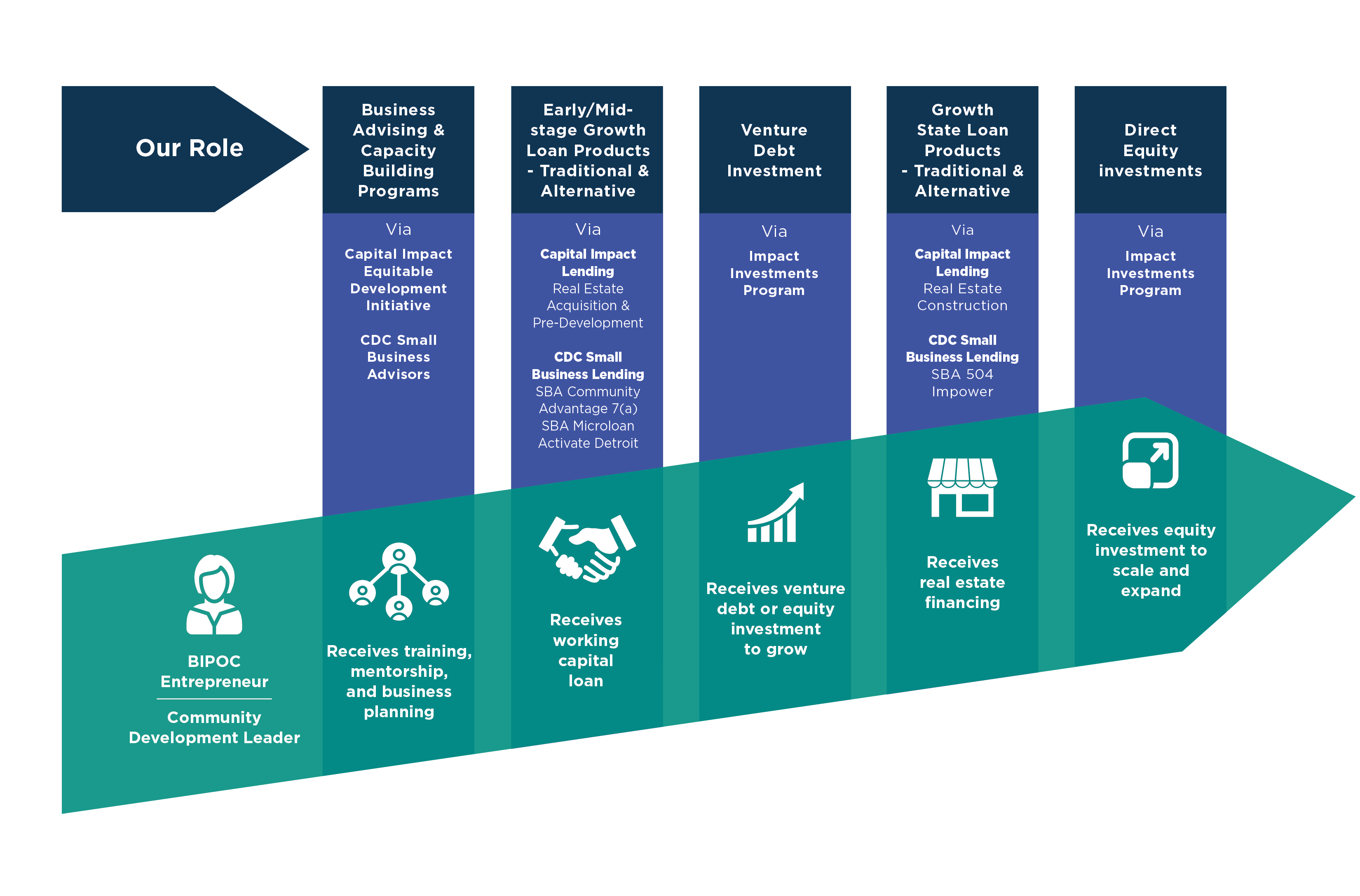

YOUR CHEAT SHEET: 2020 SBA 504 SOP UPDATE

Whether you are a lender or a small business owner considering a building purchase, our SBA 504 SOP Cheat Sheet is a quick and easy way to get familiar with the recent changes to the program.

The SBA has released SOP 50 10 6. The SOP (standard operating procedures) is a rulebook that evolves each year to address new industry issues.

The new SOP is applicable for all new loans beginning October 1, 2020.

This year’s SBA 504 SOP revisions touch on multiple topics including eligible passive companies, loans to employee stock ownership plans, insurance requirements and more.

The most notable change is around businesses owned by non-U.S. citizens, said Mike Owen, chief credit officer at CDC Small Business Finance, who’s been a leading SBA 504 lender since 1978.

“When you’re unsure about an SBA 504 policy, always default to the SOP,” Owen said.

“It’s a guide that is continually refined and revised,” he added. “You’ll want to make sure whatever decision you make in a lending context with an SBA product, it’s in alignment with this federal document.”

As the document is lengthy and detailed, we encourage you to connect with your CDC Small Business Finance SBA 504 loan expert with any questions and for clarification. Our team does a deep dive into the details so they can best serve you and your clients.

Here are key changes to be aware of from the 2020 SOP update.

Ease of Use

The new SOP is now in Microsoft Word format instead of an Adobe PDF. The new format makes it easier for users to cut and paste content along with improved search features based on topics or headings.

Affiliation Based on Franchise, License, Dealer, Jobber, and Similar Agreements

The operating or administrative agreements the operating company operates under for licensing or brand usage will now be collected if the agreement has not been previously approved and identified on the SBA Franchise Registry. In addition, contact information for any issuer that is not on the SBA Franchise Registry needs to be provided.

If documents are not readily accessible or the operating company is not cleared on SBA Franchise Registry, plan for additional clearance/loan process time given need for legal review and acceptance.

Demonstrate the Need for Desired Credit

For credit elsewhere, a general guide acceptable to the agency to evaluate personal resources of owners’ is through a personal liquidity test. Lenders can also elect to consider owners’ age and status to future retirement. A lender could demonstrate cash reserves for future retirement savings determining sufficiency for a self employed person or cash liquidities dedication to business and/or personal expenditures elsewhere to show applicants’ availability of cash justifying needs elsewhere to help meet credit elsewhere requirements.

Eligible Passive Companies

Pay close attention to these rules. The SBA is monitoring for any willful non-compliance.

Requirements: updating existing lease(s) if an existing EPC is used and lease is in non-compliance structure, formation of an SBA eligible EPC entity in compliance with SOP, minimizing estate tax planning options to adhere to SBA guidelines. If a borrower includes a spouse or “minor children” and the composition of aggregate family ownership is 20% or more, it will trigger personal guarantee requirements.

Loans to Employee Stock Ownership Plans (ESOPs)

With aging baby boomers and post-COVID strategy business exits, transfer of business ownership and strategic estate planning moves may become more prevalent and is important to document. Collection of information is essential with use of 401k monies and/or ESOP cooperative strategies and ROBS (Rollovers for Business Start-Ups). ROBS are now being used more for cash deployment given 401k tax strategies are being negatively impacted by government personal tax rules changes. Applicants are also deploying tax-deferred income sources out of a 401k to a business strategy.

Businesses engaged in any Illegal Activity

Sales or distribution of THC derived digestive or medicinal products are ineligible. CBD creams or oils strictly derived from Hemp which DO NOT include THC may be acceptable.

Prior Loss to the Government

A defaulted student loan is no longer an automatic SBA disqualification. Applicant(s) credit history will be evaluated as a whole. It will be viewed like any other defaulted credit payment in their past. A holistic view of how the potential borrower currently manages their credit will inform approval. There is now more flexibility from the SBA in approving this type of candidate.

Delinquent Federal Debt

The new SOP offers further definition when a debtor is: dealing with a creditor release, on a court ordered creditor plan, on an underwritten payment plan, or has been issued an Offer in Compromise (OIC) — all with a Federal Agency. If these apply and the applicant(s) is current in any of these plans the debts are not considered delinquent by the SBA.

Important to note, if the Federal Agency, under any of these payment plans, incurred a loss of original principal balance that is a loss to the Federal Government, the candidate is ineligible for SBA assistance. However, if the loss is rectified, they can be considered eligible for new SBA debt coupled with the same holistic view justification of credit risk based on how the applicant(s) manage credit after the loss.

Businesses Owned by Non‐U.S. Citizens

Foreigners with majority ownership of a U.S. company are no longer eligible for SBA assistance even though they pay U.S. business taxes and likely employ U.S. citizens. When foreign nationals are involved with an application, exploration of their ownership and control with OC, EPC or affiliated entity to the OC/EPC is necessary.

Restrictions on Uses of Proceeds

There is now an exception that SBA will consider in its decision for eligibility in the new SOP if there was job loss when an Operating Company moved to a new community. Applicant(s) need to provide written documentation that justifies the job loss that resulted from moving to another community to buy their building. The Applicant(s) need to show that, without the move, the sustainability of the company would be compromised.

504 Loan Program Fees and Use of Agents

Any fee paid to an agent, by the borrower or by a CDC lender, is tied to the interim loan or debenture. Transparency is required and is documented in SBA form 159.

Guaranties

SBA is closely monitoring compliance with aggregate ownership rules. Important to understand that if for estate planning purposes, a borrower includes a spouse or “minor children” within ownership, and the composition of aggregate family ownership is 20% or more, it can trigger personal guarantee requirements for the family member tied to OC operations.

Personal Life Insurance Requirements

There is no relief offered on life insurance for Operating Companies owned by sole proprietors, single-member LLC’s or continuation or continuity of business is predicated on this individual’s involvement with the business.

Historic Properties

Methodology has been updated by the agency through Notice that uses two forms of property evaluations – SBA form 2481 based on age of the property and no construction proposed or the completion of Section 106 based on age property and use of funds involves construction with CRE acquisition.

Eligible Uses of Proceeds

Using the public policy goal for exporting will require the lender to document the Operating Company can technically sell products outside of the US and operate as an exporter.

Stumped by the latest SBA SOP updates and what they mean for you? CDC Small Business Finance, a longtime leader in the SBA 504 field, can help you understand the latest policy changes with ease. Reach us at loaninfo@cdcloans.com or (619) 243-8667.

Are you ready to buy a building now? We have a team of in-house loan experts who can help. This link will take you directly to our SBA 504 loan officers who service all of California, Arizona and Nevada. Reach out to one of our loan experts today.

STAY CONNECTED

Get the latest small business news and tips: