Key Messages

- The SBA 504 Loan Program facilitates long-term, fixed-rate financing for ground-up construction, minor/major renovations, tenant improvements, or purchasing commercial/industrial property. This program typically requires only 10 percent down, with 40 percent funded by an interim lender and 50 percent by a conventional lender, providing a cost-effective option for expanding businesses.

- Approval and funding timelines are influenced by the scope of the work involved and obtaining thorough documentation. It’s essential to partner with the lender providing the construction/improvement loan to review site plans, contractor bids, and scopes of work right from the beginning to minimize the need for rework at the end of the project.

- Closely monitoring construction draws and change orders or working with a third party fund control company are crucial for protecting interim lenders. They help ensure that completed improvements are verified, lien waivers are tracked, and costs align with the approved budget.

- By partnering early with CDC Small Business Finance, lenders can better manage risks, anticipate the needs of borrowers, and keep improvement projects on schedule from the selection of bids, through changes in the costs of the project and timelines to ensure a timely 504 Debenture takeout within the Interim Lenders maturity of their loan.

Have a borrower in need of SBA 504 tenant improvement financing? Reach out to our 504 loan officers to check eligibility and keep your project on track.

Many borrowers looking to purchase older or unfinished buildings often require interior renovations before they can start operations. These renovations are typically referred to as tenant improvements. SBA 504 financing can assist with these upgrades, but only when they are made by the borrower in the commercial property they will own and occupy.. Since these commercial real estate projects involve permits, phased construction, and multiple draw requests, lenders usually seek clear guidance from the outset.

CDC Small Business Finance, part of the Momentus Capital branded family of organizations, collaborates with lenders and the small business borrower to verify project eligibility, assess timelines, and manage the necessary documentation throughout the project to ensure a smooth and timely funding..

From the time the lender is structuring the loan, finalizing contractor bids and all the way through closing, early coordination with CDC Small Business Finance helps commercial real estate borrowers understand what qualifies for eligible SBA financing. Additionally, it provides lenders with a clearer view of project timelines, occupancy requirements, and facilitates a smooth transition from interim financing to the SBA 504 takeout.

With this solid foundation and early partnership, CDC Small Business Finance can identify and help prevent delays when the scope of the improvement changes during construction. This allows lenders to assist their borrowers in creating a smoother process and navigating their construction with greater confidence.

Understanding How SBA 504 Tenant Improvements Work

Understanding how SBA 504 tenant improvements work is crucial for borrowers and contractors. The term tenant improvements refers to interior renovations done within the space that the borrower will occupy in the purchased property. It’s important to note that improvements for third-party tenants do not qualify.

As Vice President of 504 Loan Processing and Closing, I always advise that since the borrower must occupy 100 percent of the improved space, it’s vital to identify early on which parts of a building are eligible for 504 financing.

Eligible improvements can include HVAC systems, plumbing, electrical upgrades, fire and life safety enhancements, accessibility modifications, framing, and interior finishing work. These improvements are often necessary in older buildings or commercial real estate properties that have had different uses in the past. Additionally, interior improvements can represent a significant portion of the total project cost, making early assessment essential.

What can you use a SBA 504 Tenant Improvement Loan on?

| Eligible Work | Ineligible Work |

|---|---|

| Borrower-Occupied Interior Work Framing, drywall, ceilings, flooring, interior doors, paint, or insulation | Improvements Inside Non-borrower Tenant Suites Cosmetic upgrades for rental tenants or improvements benefiting another business |

| Mechanical & Utility Upgrades HVAC installation or replacement, electrical rewiring, or plumbing upgrades | Third-Party Systems Specialty systems for a separate tenant or equipment serving a tenant’s exclusive use |

| Life-Safety & Code Compliance Fire sprinklers, alarms, ADA upgrades, seismic upgrades, or accessibility work | Non-Operational Enhancements * Décor, displays, loose furnishings, marketing installations or signage not required by code |

| Permanent Fixtures Built-in counters, millwork, fixed casework | Movable Furniture * Tables, chairs, décor, removable shelving |

| Construction Draws (Verified) Progress-based disbursements, site-verified completion, or unconditional lien waivers | Unverified Draws Work submitted with missing documentation or costs that do not match the approved scope |

*Non-operational Enhancements and Movable Furniture are not covered unless allocated as a Furniture, Fixtures, and Equipment cost in the original loan structure. If a borrower adds them to the scope of work after loan approval, the items would need to be reviewed for eligibility and corrections made to the SBA Terms and Conditions. Thus causing a potential delay in the funding of the debenture.

Some projects start as straightforward tenant improvements, but the scope can change once bids come in or walls come down. When that happens, the contractor issues a change order, which is a formal update to the scope and cost. The interim lender and CDC Small Business Finance will then conduct a re-review using the updated plans, a revised project cost breakdown (including sources and uses), and all the necessary permits, invoices, and lien waivers. This ensures that the work is still eligible and within the structure presented at the time of SBA approval. If the changes are substantial (e.g., they affect eligibility, occupancy, or the approved budget), underwriting may need to get involved, and a formal loan modification will need to be issued before the next draw request is approved.

Work That May Be Eligible, But Requires Additional Review

| Potentially Eligible Work | Why It Takes Longer / What’s Needed |

|---|---|

| Shell Improvements Supporting Borrower Space Roof repair, exterior structural work, or façade updates tied to borrower use | Needs updated plans/site details and cost allocation so the work is clearly tied to the borrower-occupied portion and isn’t an exclusive benefit to leased-out suites. |

| Specialized Operational Build-Outs Food-prep, lab, medical plumbing, or manufacturing or light-industrial areas | Requires a detailed scope, permits, and documentation showing the improvements are permanent and directly support the borrower’s operations. |

| Soft Costs Architectural and engineering fees, permits, inspections, or reasonable contingencies | May require additional documentation or revisions so costs are reasonable, permitted, and fully supported by invoices and lien waivers. |

| Change Orders Affecting Eligibility Changes shifting work into ineligible areas, owner occupancy or the approved budget | Often triggers a review from underwriting (and sometimes a loan modification) if there is an increase or significant decrease to the project. Review with the Interim Lender of the proposed change order, revised scope/bids, and an updated project cost breakdown before additional draws are approved. |

Understanding the Importance of Occupancy Requirements

SBA 504 occupancy rules play a crucial role in tenant improvement projects. To qualify for an SBA 504 loan, borrowers need to occupy at least 51 percent of an existing building or 60 percent of new construction. These occupancy levels dictate which improvements can be financed.

During the review process, the funds can only be used for the borrower’s portion of the building. They can improve the overall shell, but borrowers can’t improve the space they’re leasing out to other non-affiliated businesses. Since occupancy impacts eligibility, it’s essential for commercial real estate lenders to verify site plans, proposed scopes, and contractor bids during the initial application phase.

Additionally, changes to project scopes can influence eligibility. Significant alterations can make it “almost like a brand new loan.” Therefore, early collaboration among lenders, CDC Small Business Finance, the contractor, and the borrower is vital to avoid delays. This proactive approach also minimizes rework caused by change orders that could affect occupancy or the overall budget.

Ensure Your Borrower’s Tenant Improvement Project Meets SBA 504 Requirements

Consult with our SBA 504 experts to help your borrower stay on schedule with their improvements.

How Construction Draws & Fund Control Support Lenders

Many tenant improvement projects require funds to be released in stages. These are called construction draws or draw requests. CDC Small Business Finance works with the interim lender throughout the construction/improvement process , and monitors the project’s progress to ensure timely funding/take out of the Interim Lender Loan. This approach safeguards the lender’s interests and helps ensure the interim loan is paid off as anticipated, and within their Interim Loan maturity.

Every SBA 504 loan requires temporary funding provided by the interim lender before the 504 debenture is funded. This interim financing covers the time between real-estate/land closing and project completion. Lenders remain in this interim position until all construction and improvements are completed, loan funds are fully disbursed, proper documentation is received, and the SBA debenture has been funded.

Once the work is completed, our internal construction team will work directly with the interim lender and the borrower to confirm the proper documents are in order and meet all local regulations and SBA requirements. Additionally, we confirm borrower occupancy prior to the SBA loan being finalized.

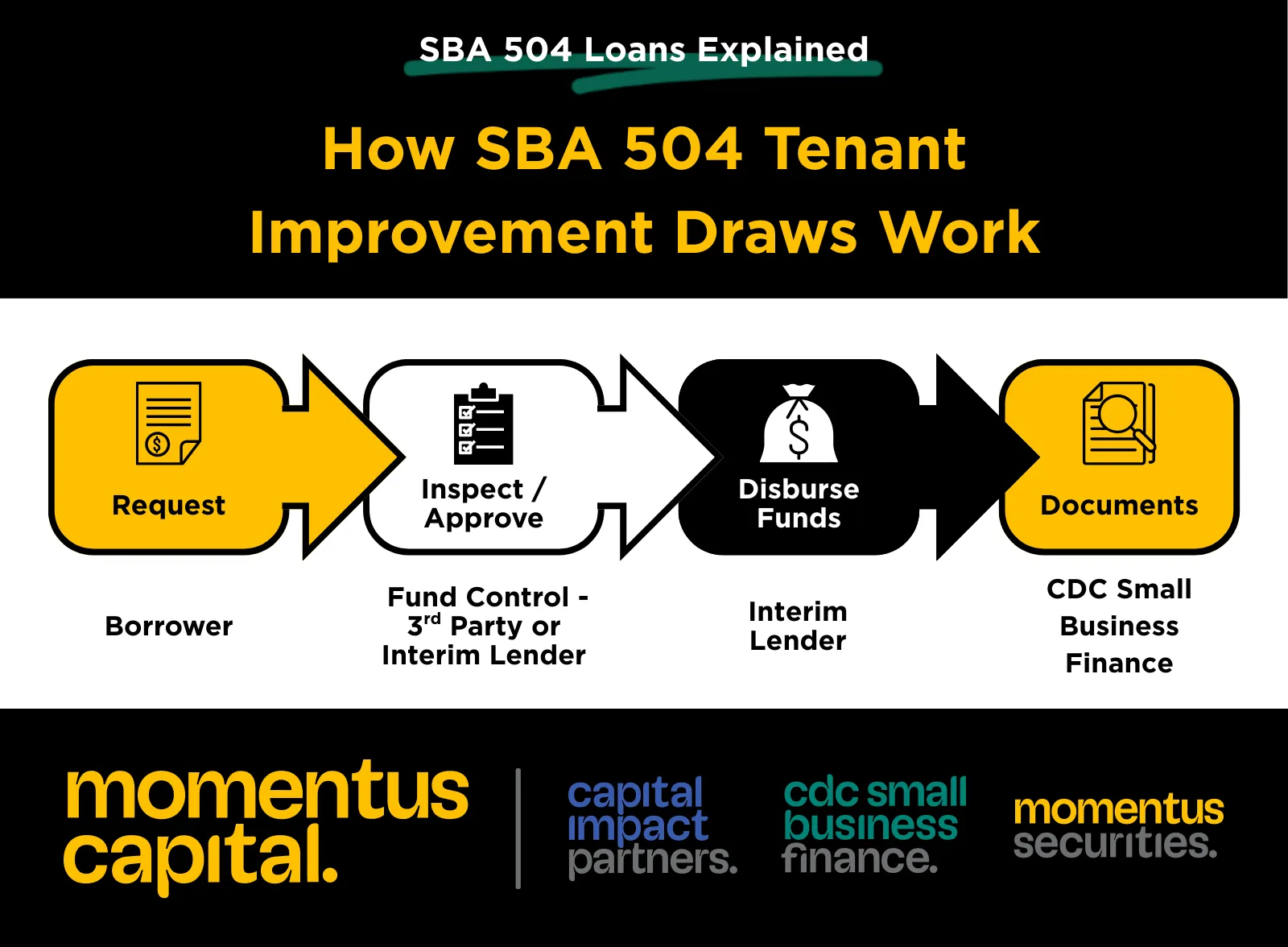

Each draw goes through four main steps:

- Request: The borrower or contractor submits invoices, schedules, and support documents directly to the Interim Lender (Construction Loan).

- Inspect and Approve: The Interim Lender or 3rd Party Fund control verifies progress, collects lien waivers, and confirms costs align with the approved scope.

- Disburse: Interim lender releases funds as work is completed and usually holds onto the final retention until a final signed-off inspection or Certificate of Occupancy is obtained.

- Documentation: CDC Small Business Finance’s internal construction team works with the Lender and Small Business Borrower to verify all required documentation meets SBA requirements in order to proceed with the funding of the debenture.

Lien waivers play an important role when the SBA 504 debenture funds. These are legal documents from a general contractor or vendor confirming they have been paid for completed work and waive any right to file a mechanic’s lien.

While a lien can still be filed in some situations, most often by a subcontractor who has not been paid, CDC Small Business Finance advises that any lien waivers that have been filed must be properly released to help ensure a clean title and funding of the Debenture. Addressing these issues early allows the parties to resolve disputes if they arise and keeps the project moving toward final funding without unnecessary delays.

We require unconditional lien waivers from the general contractor or each vendor if a GC was not used. Since tenant improvement projects often involve multiple subcontractors, accurate tracking prevents surprises at closing. This protects against future claims and ensures a clean title.

Change orders, formal adjustments to the construction contract that change the scope of the project, can extend timelines or increase costs. If a change impacts eligibility or occupancy, lenders should anticipate a revised review and additional documentation. Communicating early can help avoid delays in the final takeout.

CDC Small Business Finance can begin the funding process to pay off the Interim loan when:

- Documentation of loan proceeds have been fully disbursed and project costs allocated.

- The project is 100 percent complete.

- All documentation has been received from the municipalities, including a final, signed-off inspection report (if permits were required) or a Certificate of Occupancy.

- Unconditional lien waivers are received.

Managing Timelines & Interim Financing Exposure

The time it takes to process commercial real estate projects can vary based on permitting, inspections, and final approvals, which often leads to extended project schedules. Lenders should know that some jurisdictions have additional requirements that can delay things by weeks, months, or even years.

Market conditions and cost overruns can impact budgets. While a 10 percent contingency is typically standard, recent projects have occasionally gone beyond that. In such cases, the borrower will have to come out of pocket for the cost overruns as SBA only allows for a 10% contingency to be included in the project costs. This is why CDC Small Business Finance works early on and throughout the improvement/construction phase to ensure the project costs remain eligible.

Once construction is completed, final occupancy is approved by the applicable municipality, and all funds are disbursed, lenders should anticipate a 60- to 90-day period for final funding after the certificate of occupancy is issued. Maintaining clear communication during this phase can help ensure a smoother transition to the SBA 504 takeout.

Since interim financing remains in place until all work is finished, lenders benefit from clear communication and realistic project planning. CDC Small Business Finance plays a crucial role in setting expectations early, allowing lenders to monitor timelines more effectively.

Why Lenders Work With CDC Small Business Finance

Tenant improvement and construction projects involve several moving parts. CDC Small Business Finance’s internal support team is an extremely strong and knowledgeable back office. We are intimately involved, constantly in communication, and managing expectations. This guidance helps lenders stay informed about the timeline of the Debenture funding and what the next steps are to begin the funding process for the borrower. ls.

When lenders partner early in the loan process with CDC Small Business Finance, they can better anticipate borrower questions, avoid delays during closing, and reduce interim exposure throughout the construction period. This guidance not only helps CDC Small Business Finance to stay consistent with final approvals, it allows lenders to know when the interim loan is paid off and replaced by the permanent loan.

Still have questions about tenant improvement eligibility or 504 documentation?

These FAQs cover the most common issues lenders encounter.

What tenant improvements/leasehold improvements are eligible under an SBA 504 loan?

Eligible improvements should enhance the space occupied by the borrower’s business, including HVAC, electrical, ADA upgrades, plumbing, flooring, and structural modifications. Improvements made for third-party tenants do not qualify.

What’s the difference between tenant improvements and leasehold improvements according to SBA guidelines?

While these terms are often used interchangeably, they actually refer to different ownership scenarios and eligibility criteria. Tenant improvements generally refer to renovations made to a building that the borrower owns and occupies, which aligns with the usual structure of an SBA 504 loan. On the other hand, leasehold improvements typically refer to upgrades made in a space the borrower is leasing from a landlord.

For SBA 504 purposes, financing is tied to the borrower-occupied portion of the property and must directly benefit the operating business and meet SBA occupancy requirements. Improvements intended for third-party tenants or rented suites do not qualify for 504 financing.

What documentation is required for tenant improvements in a 504 project?

As long as licensing, ownership, and medical oversight structures meet SBA expectations, common interim lender requirements include: contractor bids, detailed cost breakdowns, floor plans, permits, proof of borrower investment, invoices, lien waivers, and photo/inspection documentation for each draw.

If no fund control was used, invoices and cancelled checks will be required. At the end of the day, CDC Small Business Finance needs to show that the loan from the lender went to proceeds, all of the money was disbursed, and show where the money was disbursed.

How does fund control work for SBA 504 tenant improvements?

Fund control entails verifying completed work, reviewing invoices, tracking lien waivers, confirming eligible costs, managing draw requests, and ensuring that borrower funds are injected before 504 disbursements.

What occupancy requirements affect tenant improvement eligibility?

According to SBA commercial real estate requirements, borrowers must occupy 100 percent of any space improved with 504 funds and may lease out up to 49 percent of an existing building and 40 percent of new construction. These criteria determine tenant improvement eligibility and closing requirements.

When should lenders engage CDC Small Business Finance for tenant improvement projects?

CDC Small Business Finance advises involving them when the lender is structuring their loan and before final approval of contractor bids/invoices to ensure that improvements are eligible, documentation is accurate, and interim-lender exposure is minimized.

Next Steps for Lenders

When a borrower is getting ready for a tenant improvement project, CDC Small Business Finance can assist in confirming eligibility before construction or improvements begin. This early review helps avoid common delays and enables lenders to offer clear guidance.

Have questions about SBA 504 tenant improvement eligibility? Contact one of our 504 loan officers to review your borrower’s project before bids or work begin.