Key Messages

- SBA 7(a) Community Advantage loans can finance leased-space tenant improvements, but the lease, project scope, and documentation need to be aligned from the start.

- In most cases, underwriting cannot begin without a draft LOI/lease and a walkthrough-based TI estimate.

- Lease-term alignment (including renewal options) is an underwriting issue, not a paperwork detail.

- Fund control and construction draws protect both the borrower and the lender, but they change how contractors get paid.

- If the lease includes a tenant improvement allowance reimbursement, it should be flagged early because it can affect principal paydown and working capital disbursement timing.

Do you have a draft LOI/lease and an initial TI budget? Contact CDC Small Business Finance for an early review with a loan officer.

A leased space can look like the right location, but it can take weeks or even months before it’s ready to open. Essential work like plumbing, electrical, HVAC, flooring, restrooms, and other permitted work often have to be completed before the business can start operating.

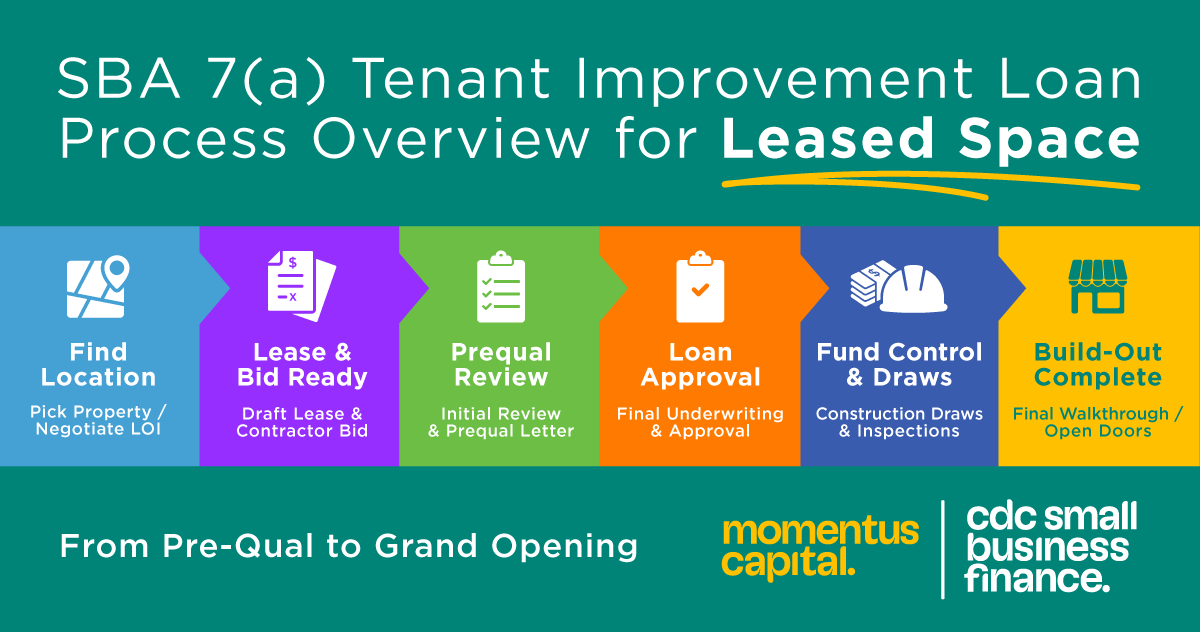

CDC Small Business Finance, part of the Momentus Capital branded family of organizations, can finance tenant improvements (TI) through the SBA 7(a) Community Advantage loan program. The key question isn’t just whether the build-out can be funded, but also what needs to be in place early on to ensure the project transitions smoothly from prequalification to closing and draws without unnecessary delays.

Most delays in tenant improvements for leased spaces typically arise from a few common issues: misalignment of lease terms, incomplete contractor bids, timing of permits, and misunderstandings regarding draws and landlord reimbursements. While these problems are not uncommon, addressing these issues early, before signing the final lease and starting construction, tends to prevent the most common delays in underwriting, closing, and fund control.

What Counts as Tenant Improvements (and Why it Matters for Financing)

When it comes to financing leased spaces, tenant improvements (also called leasehold improvements) are the modifications required to make the space usable for a business. These improvements usually encompass various build-out elements such as windows, flooring, plumbing, HVAC, electrical work, and similar work that requires a contractor or permits. Painting can be included in the TI budget, even if some of the work is done independently.

Banks and lenders treat these items as more than construction line items because TI projects are tied to permits, inspections, opening timelines, and contractor documentation. For businesses that rely on specific locations, especially customer-facing businesses, the site is part of the repayment picture, so the lease and build-out plan are underwriting issues from day one.

For borrowers considering an owner-occupied property, check out our SBA 504 tenant improvements blog.

The “Don’t-Sign-Yet” Timeline (What Can Happen Before the Lease is Final)

Many borrowers assume they have to sign the final lease before they can talk to a lender. That assumption can create leverage problems and out-of-pocket risk. We recommend starting finance discussions while working from a draft Letter of Intent (LOI) or draft lease, as long as a walkthrough-based estimate from a contractor who has actually seen the space is provided.

Once a loan officer has taken a look at the documents, they can provide a pre-prequalification letter. This letter serves as a written indication that, based on a quick review of the LOI, project scope, and TI estimate, the project seems to meet the initial financing criteria. While this can be a handy tool during lease negotiations, it’s important to remember that it doesn’t equate to a loan approval commitment and doesn’t guarantee the final terms or funding.

When the Project is “Real Enough” to Review

In practice, the deal can start moving once two things show up:

- A draft LOI or draft lease

- A TI estimate from a contractor who has walked the space

This estimate does not have to be a finalized construction contract at the prequalification stage. Instead, a rough estimate can suffice if the drawings aren’t yet complete. Underwriting may look at the upper end of the estimate to reduce the risk of underfunding the project. If later drawings push the cost meaningfully higher, the structure may need to be adjusted.

Lease Term Requirements & Landlord Documents That Can Stall a Deal

Lease term alignment is often one of the first hurdles that can slow down a TI deal, and it tends to be underestimated. Many people mistakenly believe that the borrower has to commit to staying in the space for the entire loan term. The real question is whether the borrower has the legal right to occupy the space long enough to cover repayment, which includes any applicable renewal options.

That’s why having a five-year lease with renewal options can be just as important as a longer initial term. When it comes to underwriting, the focus is on occupancy rights rather than just current intentions. CDC Small Business Finance’s Director of Credit Underwriting Nick Miluso notes that lease term alignment is about confirming that “occupancy rights support repayment, especially for businesses whose revenue depends on that specific location.”

Landlord-related paperwork can also delay a TI loan, especially when landlords need to be involved in the reimbursement process. Problems like landlord waivers and assignment-of-lease can create friction, and larger shopping centers often face delays because of the intricate property management and legal approvals that are needed for the required paperwork.

One important lease term that can significantly impact a business’s runway is rent abatement. Since the permitting and construction processes can stretch on for months, it’s wise for borrowers to negotiate rent abatement early on. This way, rent won’t kick in until the business is ready to open its doors and has an inflow of cash.

Before signing that final lease, contact CDC Small Business Finance.

We can review lease term alignment, renewal options, and TI-related lease terms.

Fund Control & Construction Draws Explained (Why Contractors Do Not Get Deposits)

In leased-space TI projects, borrowers often expect a single construction check after closing. That is not how the disbursement process usually works. Fund control and draws are typically a staged reimbursement process: payment is released for verified work completed, not future work.

Here’s a simple breakdown of how fund control and construction draw sequences work:

- The work is divided into phases, like demo, electrical, framing, and finishes.

- The contractor sends in a draw request along with invoices and lien waivers.

- An inspection or verification step confirms that the work is on track.

- Once everything checks out, the lender approves the draw.

- The funds are released to the contractor, either via check or ACH, which usually takes about five to seven business days.

Nick Miluso points out that fund control is not only a lender safeguard; it’s also a way to ensure everything is on track and to gather lien documentation. “Fund control is a protection, not a hurdle,” he says. “It’s just as much a borrower protection as a lender protection. It reduces the risk of any unresolved construction issues coming to light when the business is trying to open.”

When it comes to practical issues, we often find that the friction points are more about operations than theory. Some typical examples include:

- Missing lien waivers

- Incomplete invoices

- Unapproved change orders

- Draw requests submitted before the work is finished

How the contractor relationship is structured has a direct impact on how smoothly the draw process goes. Here are the key things to keep in mind:

- Use one general contractor (GC) or prime contractor for the full build-out.

- Avoid treating the project like an owner-builder job with lots of separate payments to different subcontractors.

- Be prepared for fund control to ask for contractor licensing and insurance documents.

- Make sure to have a fixed-price construction contract (not a shifting quote/time-and-materials approach) for managing construction draws.

One of the biggest reasons for delays is the permitting process, which can lead to cash flow issues when lease payments and pre-opening costs start piling up before the construction funds are available.

Start an application or contact a CDC loan officer

to review contractor documents, fund control requirements, and draw timing.

Tenant Improvement Allowance (TIA) — A Real Benefit, but Plan for Reimbursement Rules

A tenant improvement allowance (TIA) is a financial contribution from the landlord to help with the renovations of a rented space. However, borrowers often think it covers more than it actually does and are left waiting longer than expected for the funds. A TIA won’t cover the entire budget for the build-out, and the reimbursement happens only after the work is done. There might be a need for inspections and lien waivers before the money is released. Additionally, soft costs such as permits, design, engineering, and some city fees often fall outside the contractor’s quote and aren’t part of what the landlord will cover.

A TIA reimbursement is more than just a lease benefit; it also ties into how loans are structured. When the funds from an SBA 7(a) loan are used to cover improvements, and the landlord later reimburses those expenses, there’s often a specific way to manage that reimbursement. Typically, it involves paying down the principal, unless the lender has documented a different approach that meets SBA guidelines.

Leased-Space TI Readiness Checklist

The quickest TI deals tend to happen when the borrower has a clear understanding of the scope, timeline, and budget. This means working with one general contractor, having a realistic scope of work (including a contingency plan), and treating permits as key factors in the timeline.

- Draft Letter of Intent (LOI) or lease that clearly outlines any renewal options

- Walkthrough-based estimate from a general contractor or prime for the entire project

- Budget that includes soft costs, not only the contractor quote (permits, design/engineering, utility/city fees, deposits as applicable)

- Contingency built into the TI budget (often 10 percent)

- Permit timing treated as an important scheduling factor

- TIA language identified and flagged for underwriting review, if applicable

- No demo or construction started before lender approval, closing, and all required documents in place

Leased-space TI financing is manageable, but the sequence drives the timeline. Borrowers who bring a draft LOI or lease, a walkthrough-based TI estimate, and a realistic budget into the process early give underwriting and fund control a cleaner path.

FAQ

Can SBA 7(a) Community Advantage pay for tenant improvements?

Yes. SBA 7(a) Community Advantage can finance tenant improvements for leased-space build-outs, as long as everything meets the necessary underwriting, documentation, and project control requirements.

Does a borrower need to sign the lease before applying for an SBA loan?

No, the final executed lease is not required before approval. The loan process can continue with just a draft Letter of Intent (LOI) or a draft lease, along with a TI estimate based on a walkthrough.

What is fund control and why are draws used?

Fund control is a third-party-managed disbursement process used to release TI funds in stages after completed work is verified. Draws help document progress, support inspections, and collect lien waivers/releases.

Why won’t the contractor get a deposit upfront?

In our fund-controlled TI loans, payments are released through draws after verified work. So, contractors typically do not receive traditional upfront deposits. Contractors should understand this before the project starts.

What is a tenant improvement allowance (TIA)?

A TIA is a landlord contribution toward improvements in leased space. It is often tied to permanent improvements and may not cover soft costs, permits, FF&E (furniture, fixtures, and equipment), signage, or working capital. It is also reimbursed after work is complete, not paid upfront.

If the landlord reimburses TI costs, what happens to that money?

In many cases, the reimbursement is applied to the SBA loan (principal paydown), unless the lender has documented an allowed alternative use under SBA requirements, such as supported working capital needs. The key takeaway is to flag the TI allowance early so the lender can structure it correctly before closing.

What causes delays in leased-space TI financing?

The most common delays are permit delays, incomplete draw paperwork, unapproved change orders, budget gaps (especially missing soft costs/contingency), and contractor/setup issues such as multiple contractors instead of one GC or prime contractor.

Ready to discuss a leased-space build-out?

Contact CDC Small Business Finance or start an application to review next steps, documentation, and likely timing

This post is for general educational information and is not legal advice. Borrowers should consult qualified legal counsel on lease terms, landlord agreements, and legal obligations.