Key Messages

- Businesses that legally require a medical director often face SBA eligibility issues if that individual is treated as a key management employee.

- The SBA may require key managers to personally guarantee a loan, even if they own 0 percent of the business.

- Third-party medical directors or MSA structures can reduce this risk by making medical oversight replaceable.

- CDC Small Business Finance lends nationwide to med spas, IV hydration clinics, and wellness businesses with compliant structures.

- The earlier a business reviews their structure with a lender, the easier the SBA loan process becomes.

Ready to see if your structure works for SBA?

When opening a med spa, IV hydration clinic, health center, weight-loss practice, or other wellness business, medical oversight is often a legal requirement. In many states, these businesses can’t even get off the ground without a medical director or supervising physician on board.

The tricky part for founders usually comes when this requirement bumps up against SBA loan medical director rules.

At CDC Small Business Finance, part of the Momentus Capital branded family of organizations, we often talk to borrowers, many of whom are nurses, registered nurses (RNs), or nurse practitioners (NPs), who are caught off guard to find that their SBA application has stalled not because of credit, cash flow, or experience, but because the medical director is viewed as a key management employee who isn’t willing to guarantee the loan. This is one of the most common issues CDC loan officers come across, especially with start-ups that already have contracts in place. As Stacey Sanchez explained, “This is the biggest pain point we see. They call us, they have all the stuff lined up but need financing. Then they realize too late how the medical director is viewed by the SBA.”

The silver lining? With the right set-up, many of these businesses can actually qualify for SBA 7(a) Community Advantage loans.

Does Your Business Need a Medical Director?

Whether or not a business needs a medical director really depends on the state laws and the services provided. A medical director is a licensed physician who oversees the clinical side of a healthcare or wellness practice to help ensure services are delivered safely and meet medical standards.

While they may not be involved in delivering services or running the business, the medical director provides required physician oversight, establishes clinical protocols, and helps keep the business compliant with state laws and regulations. If a clinic offers medical services, especially those that involve prescriptions or medical procedures, most states will require a medical director.

This comes up frequently in SBA applications for med spas and wellness clinics. Megan Stuit, a CDC Small Business Finance loan officer who reviews these deals nearly every other week, often has to walk borrowers through the medical director requirements early in the process. “The issue is that a nurse or other practitioner can provide the service, but the state still wants a medical director overseeing the operation, even though the medical director really doesn’t do any of the services.”

Common Businesses that Require a Medical Director

- Medical spas and aesthetic clinics

- IV hydration and wellness infusion clinics

- Weight-loss clinics using prescription medications

- Health centers not owned by a physician

- Nurse-owned or NP-led regulated wellness businesses

Once it’s determined that a medical director is necessary, the SBA wants to know if that business is reliant on one specific physician to operate.

What the SBA Looks at When a Business Needs a Medical Director

When lenders are looking at SBA 7(a) Community Advantage loans for regulated wellness businesses, they focus less on the specific title of a role and more on whether the business can operate without that person. They’re also interested in who has the final say on important decisions. From the SBA’s standpoint, any person that a business can’t legally function without is important.

If a clinic needs a medical director to operate, SBA lenders may view that individual as a key management employee. Under SBA rules, key managers often have to personally guarantee the loan, even if they don’t own the business. This means lenders must determine if the business is heavily dependent on one person.

Many wellness businesses are unclear in how SBA underwriting evaluates roles tied to required medical oversight. Under SBA guidelines, individuals who either own 20 percent or more of the business or are considered key management employees are required to guarantee the loan. As Stacey Sanchez explained during a recent review of these scenarios, “That key management employee piece is the line that catches them. The medical directors aren’t owners. But if they’re considered a key management employee, and that medical director doesn’t want to be responsible for the loan, the business doesn’t qualify.”

Key Questions to Think About Usually Include:

- Is a medical director required by state law?

- Is the business reliant on a specific physician to function?

- Who makes the day-to-day business decisions?

- Who oversees the clinical side versus the administrative side?

Many borrowers think that since the medical director is merely a licensing formality, it won’t impact the underwriting process. However, lenders need to assess if the business can legally and practically keep running if that person were to leave. This is often discovered later than it should be. As Megan noted, “Oftentimes, it’s too far along by the time they ask the question. They already have the doctor in place, and now we’re trying to work backward.”

If the business can’t operate legally without that one doctor, and that doctor isn’t willing to back the loan, it can jeopardize eligibility, turning what could have been a manageable issue into a frustrating delay or even a denial.

Already working with a third-party medical director company?

See how much you may qualify for with an SBA 7(a) Community Advantage loan.

How Third-Party Medical Director & MSA/MSO Models Help

This is where third-party medical director companies, along with Management Services Agreement (MSA) or Management Services Organization (MSO) structures, really come into play.

An MSA is a contract used by nurse-owned and non-physician-owned medical spas, IV hydration clinics, and other regulated wellness businesses to help meet state licensing and medical oversight requirements, without giving ownership to a physician. The MSO acts as the behind-the-scenes operating company.

In this set-up, the borrower is the MSO and manages the clinic on a daily basis. This includes everything from operations and staffing to scheduling, patient experience, billing, marketing, facilities, and overall business strategy. The owners are typically nurses, nurse practitioners, or other health care professionals who are qualified to run the business but, according to state law, need a physician involved for clinical oversight.

From a lending perspective, this can significantly alter the underwriting process because the medical director role becomes more interchangeable, even while clinical oversight remains intact. Well-structured MSAs enable med spas to function efficiently, allowing the MSO to concentrate on business growth while the third-party medical director company ensures compliance and clinical oversight.

These structures tend to work best when they are set up early and reviewed with both licensing and lending in mind. As Stacey explained, “So far, those MSAs, third-party contracts, aren’t required to be approved by the SBA. That flexibility makes a difference when we’re reviewing the structure.”

This distinction often allows lenders to concentrate on the business fundamentals rather than getting stuck on one individual’s willingness to guarantee the loan.

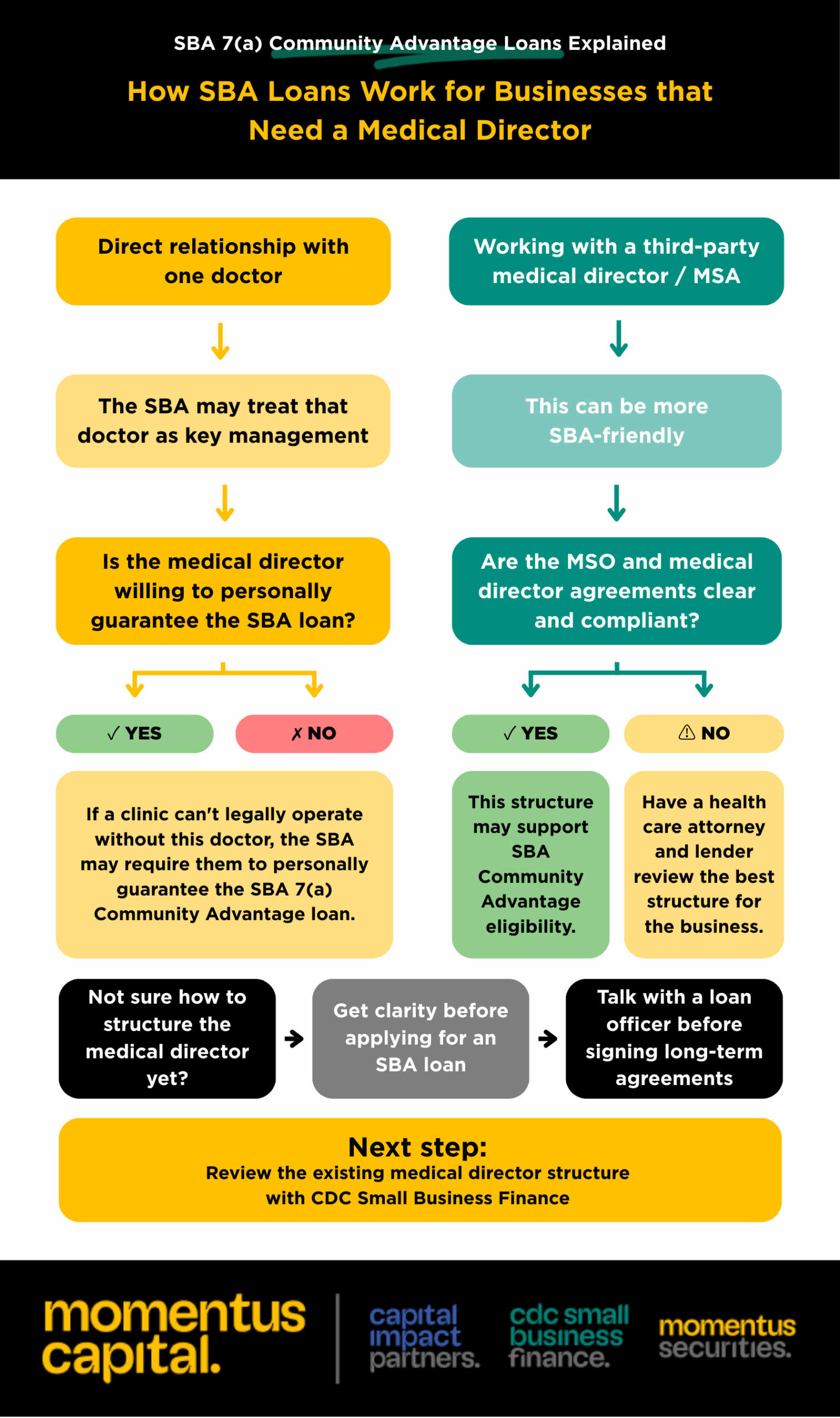

Here’s a handy flowchart that outlines the key decision points lenders consider when looking at SBA 7(a) Community Advantage loans for businesses needing a medical director. It captures the common scenarios loan officers encounter, like direct contracts with individual physicians, third-party medical director companies, and MSO structures. Plus, it points out where eligibility issues often pop up.

If a med spa or wellness center is still figuring out how to set up their business, this tool can provide guidance on when it’s wise to hit pause and consult with a lender before locking into long-term agreements, rather than running into problems after submitting loan applications.

Before You Apply: Checklist for SBA-Ready Medical Director Structures

Before applying for an SBA 7(a) Community Advantage loan, it’s a good idea to put the business structure to the test, just like a lender would.

Borrowers who navigate the underwriting process smoothly often have a clear understanding of whether a medical director is legally necessary, how that role is set up, and who has the final say in business operations. Loan officers consistently stress that having clarity from the start is more important than having everything perfectly documented on day one.

That’s why taking a close look at the med spa or wellness center’s structure early on can save a lot of time down the road, especially if it’s a start-up still working out contracts.

Before applying for an SBA 7(a) Community Advantage loan, make sure the answer is a confident “yes” to most of the following:

- The state’s legal requirement for a medical director is understood.

- The medical director relationship is documented and compliant.

- Ownership and control are clearly defined.

- MSA or medical director agreements have been reviewed by an attorney who routinely handles corporate practice of medicine (CPOM) structures.

- The business structure has been discussed with a lender before submitting an application.

Doing this groundwork can save months of delays or even help avoid having an SBA loan declined.

When to Talk to a Lender If a Business Needs a Medical Director

The best time to talk with a lender is before the medical director or MSA agreements are finalized.

Once those contracts are signed, making changes can lead to extra legal work and delays. Loan officers often encounter borrowers who have to restructure their agreements simply because the initial contract didn’t meet SBA requirements. Timing is often the deciding factor. As Stacey explained, “If we see it early, we can usually guide businesses. Once agreements are signed, that’s when it gets hard.”

For wellness businesses that are regulated, having that early discussion can mean the difference between a smooth approval process and an unnecessary decline.

Not sure if your set-up will pass SBA’s key-employee test?

An SBA 7(a) Community Advantage loan officer can walk you through your options.

SBA 7(a) Community Advantage Medical Director Rules Q&A

Here are some of the most common questions we hear about SBA loan medical director requirements.

How does a medical director affect SBA loan eligibility?

If a medical director is essential for operations, the SBA might consider them a key management employee. This could mean they need to act as a guarantor for the loan.

Does my medical director have to guarantee the SBA loan?

Sometimes, yes. It really depends on how crucial that person is to the operations and how the relationship is set up. There are third-party medical director companies and structures like Management Services Agreements (MSA) or Management Services Organizations (MSO) that can help avoid naming a specific individual on your SBA loan. It’s a good idea to chat with a loan officer to understand what’s needed.

What is an MSO/MSA and how does it help with SBA compliance?

In simple terms, an MSO is the business entity that manages the non-clinical aspects of the clinic, while the physician oversees the clinical side. An MSA is a contract used by non-physician-owned, regulated wellness businesses to fulfill state licensing and medical oversight requirements. An MSA can provide the necessary medical oversight while keeping business operations separate, which might lower the SBA’s key-employee risks that require a medical director to guarantee a loan.

Can nurses or NPs qualify for SBA 7(a) Community Advantage loans?

Absolutely! Many do, especially when their business structure properly addresses the medical director requirements.

Are med spas and IV hydration clinics eligible for SBA loans?

Yes, as long as their licensing, ownership, and medical oversight structures meet SBA expectations.

Ready to Finance a Wellness Business With an SBA 7(a) Community Advantage Loan?

Having a medical director doesn’t automatically disqualify a business from SBA financing. But how that relationship is structured matters.

With the right setup, many med spas, IV hydration clinics, health centers and wellness businesses successfully use SBA 7(a) Community Advantage loans to launch and grow. The key is understanding SBA expectations early and building the business structure around them.

Still planning your clinic? A short conversation now can help you avoid structuring issues that delay SBA approval later. Connect with a Loan Officer today.