SBA 504 Commercial Real Estate Loans

Why rent when you can own?

You can use an SBA 504 loan to buy, construct or improve commercial real estate or to purchase heavy equipment. Talk to one of our SBA 504 loan experts to learn how you can take advantage of a long-term, fixed rate, and low down-payment (only 10%) SBA commercial real estate loan.

Many of our borrowers find that their loan payment ends up being less than what they were paying in rent. See below for details on rates, loan amount, eligibility, loan structure, key benefits, and more.

Today’s Rates*

Current SBA 504 25 year standard rate: 5.722%

Current SBA 504 25 year refi rate: 5.725%

Current SBA 504 25 year manufacturing rate: 5.480%

Current SBA 504 20 year standard rate: 5.783%

Current SBA 504 20 year refi rate: 5.786%

Current SBA 504 20 year manufacturing rate: 5.531%

Current SBA 504 10 year standard rate: 5.611%

Current SBA 504 10 year manufacturing rate: 5.310%

SBA 504 Loans: FAQs

See the top questions we hear from small business owners who are considering buying a commercial building. Get answers on timing, fees, and loan size.

SBA 504 rates include fees to CDC, SBA, and central servicing agent based on debenture pricing published by NADCO. The SBA 504 rates listed above are effective March 5, 2026 and change monthly with each funding cycle.

The Benefits of an SBA 504 Loan

- Preserve cash – down-payment is only 10%

- Below-market fixed interest rate

- 25, 20 or 10 year term options

- Build owner equity

- Tax savings

- No additional collateral needed

- Only 51% occupancy required

- Fixed occupancy costs

While there are multiple SBA loans that can be used for real estate and equipment, the SBA 504 loan has many advantages.

Buy vs. Lease

We’re here to answer your questions, explain the process, and help you navigate the path to getting financing to buy a building for your business.

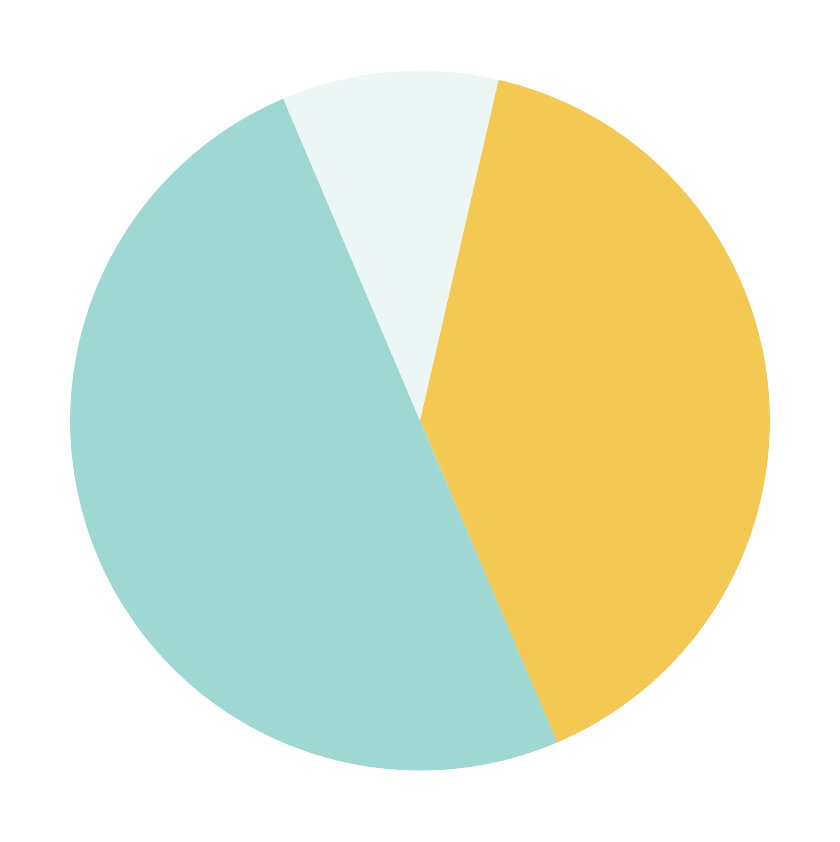

SBA 504 Loan Structure

CDC / SBA (40%)

Bank (50%)

Business Owner (10%)

How can I use an SBA 504 loan?

Purchase, Construct or Improve Commercial Real Estate

Count on knowing your occupancy costs with a below-market fixed rate

Buy & Install Heavy Equipment for Your Small Business

Get equity, tax, and cash flow advantages by owning your heavy equipment

SBA 504 Loan Eligibility Requirements

- At least 51% Owner Occupied

- For profit

- A sole proprietorship, corporation, partnership, or LLC

- Business net-worth below $20 million and a net-profit after taxes below $5 million with the last two operating years

- Business is located in our lending footprint: California, Arizona, or Nevada

Not Eligible for SBA 504? Consider Impower 95

Don’t qualify for an SBA 504 loan or traditional bank financing for commercial real estate? Our affiliate Momentus Direct Capital offers Impower 95 — a flexible way to finance owner-occupied commercial real estate with higher loan-to-value ratios and faster approvals.

| Impower 95 (Details) | SBA 504 | |

|---|---|---|

| Credit Score | ||

| Credit Score |

No minimum credit score |

Credit requirements apply |

| Occupancy Requirement | ||

| Occupancy Requirement |

Minimum 25% owner occupancy (exceptions available for businesses that benefit the community like medical providers) |

51% existing building; |

| Down Payment | ||

| Down Payment |

5%-15% (depending on property type) |

10-15% (depending on property type) |

| LTV Ratio | ||

| LTV Ratio |

85-95% (depending on property type) |

85-90% combined (50% bank + 35-40% SBA) |

| Amortization / Prepayment Penalty | ||

| Amortization / Prepayment Penalty |

Up to 30 years (helps lower monthly payments, improving cash flow) / Declining 5-1% prepayment penalty |

Up to 25 years / Declining 10 year prepayment penalty |

| SBA Eligibility | ||

| SBA Eligibility |

Flexibility around citizenship, occupancy and other standard SBA requirements |

Broad but rigid eligibility criteria with no allowance for exceptions |

Top Questions We Hear from Small Business Owners

What are the main advantages of an SBA 504 loan?

- Lower down-payment requirements – only 10%

- Long repayment terms (25, 20 and 10 year options)

- Fixed rate for the term of the loan

- Projected income is considered, not just historical cash flows

- Collateral is typically the building being financed

How long does it take to get an SBA 504 loan?

Straight purchases usually require no more than 60 days to fund. If construction is involved, this can extend the process.

What are the fees involved?

Fees vary by deal size and range from $3750-$5,000. Additional fees may apply if specific documents are required to be reviewed such as a land lease.

Can other costs be included in an SBA 504 loan?

Yes, “soft costs” (e.g. appraisals, environmental, construction interest, closing costs) can also be financed in the 504 loan, allowing the small business to preserve working capital.

How much space does the business have to occupy?

The business must occupy 51% of an existing building purchase or 60% if constructing a new facility.

What kind of equipment can be financed with an SBA 504 loan?

Long-term machinery and equipment with a useful life greater than ten years (e.g., a printing press).

What if I’m unable to qualify for an SBA 504 loan?

We understand that not all of our borrowers are able to qualify for the SBA 504 loan product due to its eligibility requirements. To bridge that gap, we’ve created the new Impower loan. Learn more here

SBA 504 Refinance Program

Refinance non-SBA guaranteed commercial real estate loans into a more affordable SBA 504 loan.

Learn more about the program:

- Key Guidelines

- Eligible Project Costs

- Expenses

- How to Evaluate Eligibility

- Steps to Qualify Existing Debt

- Loan-to-Value Limitations

Hear from Some of Our Borrowers

“When I tell people how I bought a building and was got a loan they are surprised. For me, it is the American dream.”

“We came here with very little and we got the opportunity to work hard and open our own business. Now I look back and I am very happy and very thankful for being in this country.”

“We decided to move forward with the SBA loan and to this day it’s been a great success as we were able to expand our operations, hire new people, and get us ready for the future.”