Business Loans – Know These 4 Things to Protect Your Bottom Line

Knowledge is power. This is especially true when it comes to learning the facts so you’ll know what to do to give your business the financial boost it needs to thrive.

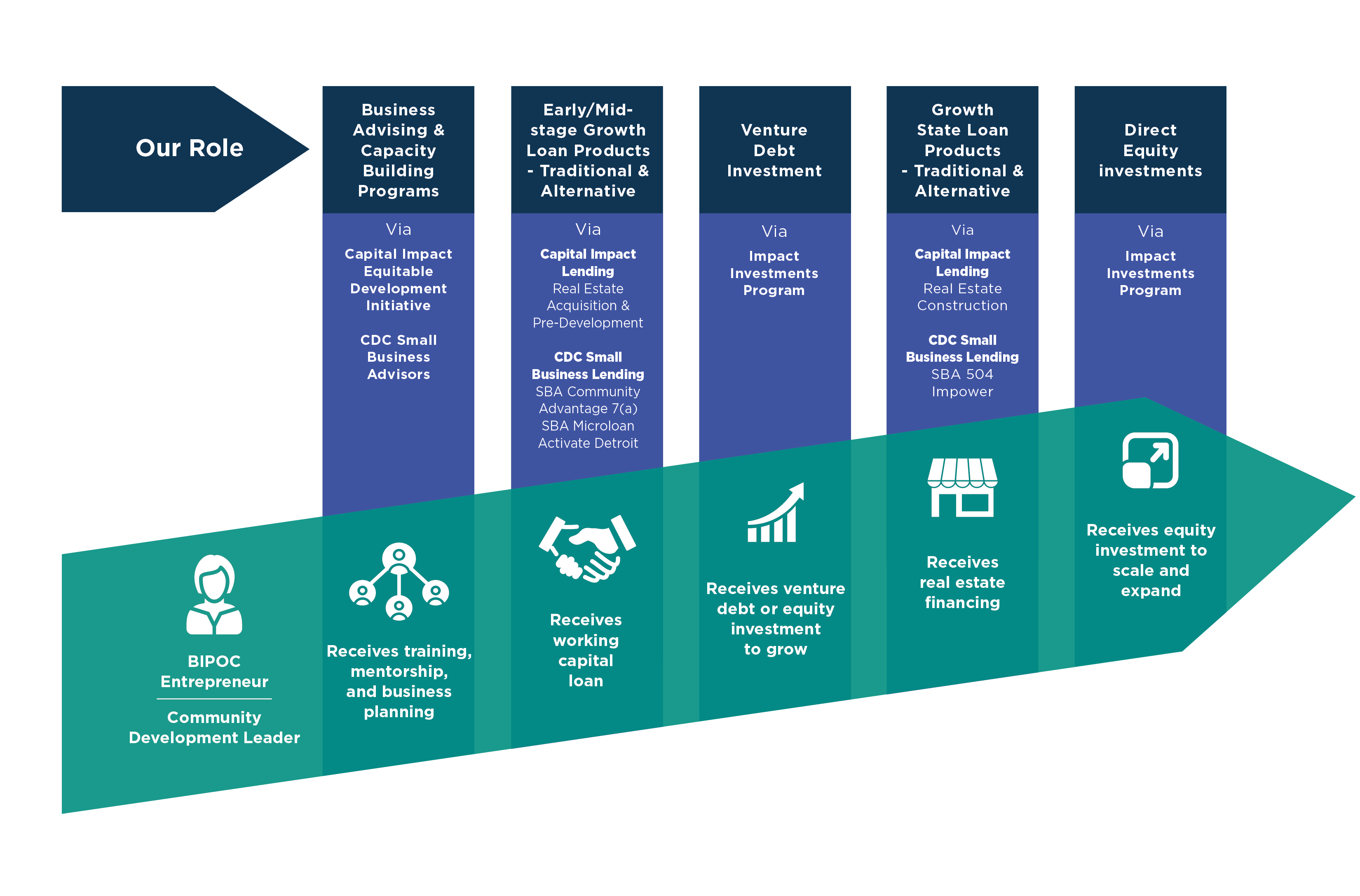

Whether the goal is to fill short-term needs, make long-term growth possible, or even to plant the seeds for a new venture, established business people and entrepreneurs alike should make an effort to become familiar with the variety of resources available to them.

One key, though, is to recognize that not all lenders are alike, nor are the types of loans they offer. Taking the steps to understand these differences can save a business lots of money – and prevent major headaches – along the way.

Related: How financing with business coaching helped beer aficionado open tasting room

That’s why we’re proud to offer our e-book “Want to Get an Online Business Loan? 10 Questions to Ask Before Committing to One,” a map to help navigate the complex financing landscape.

As we created the e-book, we were lead by four general guidelines for business owners, based on our 40-plus years of experience with small-business clients.

KNOW YOUR NEEDS

It’s best to clearly define your plans. Not only will you better serve your business, you also will impress loan officers if you can demonstrate that you know exactly where your business is going and what you need to get it there.

George Thornton had a specific vision when he launched The Homebrewer shop in the San Diego’s North Park community. He not only had a deep fascination with beer, but he also had held a part-time job at a beer supplier during graduate school. The experience added to his knowledge base.

“I was doing one thing and focusing,” George said. CDC Small Business Finance recognized his passion and expertise in deciding to offer him support.

KNOW YOUR LENDER

Online transactions are great for instant gratification, but for business owners there can be hidden costs. Be aware of the distinction between traditional lenders, like banks, versus online operations and mission-based lenders that target their services to small business clients. Finding the right fit is important.

KNOW YOUR CREDIT SCORE

Don’t assume your credit is poor! You may be surprised, and very pleasantly at that. Securing favorable terms does not require perfect credit, just good credit. One warning: Online firms may not even look at your score. But that means they’re taking on more risk and charging higher interest rates to offset it. It may be fast cash, but in the end, it’s more money out of your pocket.

THE FINE PRINT

That’s where those high rates are, for starters. If something seems too good to be true, beware. Quick financing can come with steep costs, and not just in the form of rates that dwarf credit card APR’s. There also might be pre-payment penalties that make it expensive for borrowers to pay off their loans ahead of schedule.

Related: The rewards of escaping a high-interest loan

Partners Jason Berry and Stuart Hecker joined forces to found Becker Tire and Service Center in Santa Ana. Later, they found themselves saddled with a loan that came with what amounted to an overwhelming 42-percent interest rate. After a failed attempt to use a traditional bank for refinancing, they turned to CDC Small Business Finance and secured a loan with a 7-percent rate, to their great relief.

“We were under so much pressure, having invested our life savings in the business. Twenty people still have jobs thanks to CDC,” Jason said.

HELP IS AVAILABLE

Another key for small businesses is simply knowing that whether it’s financing advice or business mentorship, support is out there.

Caterer Noelle Salinas faced a whopping loan payment of $13,000 a month, in addition to other debts. Though her Phoenix business was a success, winning local magazine honors and major contracts for high-profile celebrity parties, her debt burden had grown too large. She feared for her company.

She found the right financial path with CDC Small Business Finance.

“When I got the text that I’d been approved for the loan, I was extremely relieved,” Noelle said.

Related: Award-winning caterer overcomes challenges with affordable financing

For George Thornton, help didn’t just come in the form of a loan for his business. He accepted an adviser, CDC’s Chuck Sinks, as a condition of his SBA Microloan terms. Like many businesspeople, George also found himself with an online loan with costly terms. Chuck focused in on it immediately.

“With Chuck’s advice, we made it a priority to pay (the online loan) off first,” George said.

LENDING BASICS

CDC Small Business Finance is an award-winning business lender that strives to match you with financing that makes sense for your business.

Our e-book is one way to make sure you’re in the know when it comes to the basics of lending. Download “Want To Get An Online Business Loan? 10 Questions to Ask Before Committing to One,” for more great tips, loan definitions and even a short history lesson on lending.

Download our e-book now

In case you missed it:

Be prepared when applying for a small business loan

Business owners: Ask yourself these 5 essential financial planning questions

Beware of fast-money loan options

Here’s your safe way out of online-only debt

Before you get an online business loan, ask yourself this key question

Do you need help launching or growing your business? The experienced loan experts at CDC Small Business Finance are here to help you reach your goals. And for qualified borrowers who need financial guidance, we can connect you to our Business Advising Services Team to help you get loan-ready – for free.

Tell our experts about your business, and they’ll match you with the financing or assistance that best suits you. Let’s talk! Reach us at loaninfo@cdcloans.com or (619) 243-8667.